What is an Emergency Fund?

An emergency fund is a reserve of reasonable liquid (accessible) money that can be utilized to cover an unexpected expense. Think of it as a financial safety net! If you were to be hit with an unexpected repair bill on your primary vehicle, this reserve could be utilized if your normally available funds are unavailable or your budget is exhausted.

Emergency Fund = Peace of Mind

Emergency funds guarantee your financial safety and health. They ensure that during unexpected times of need, you do not need to dip into assets or take on liabilities to meet this new expense. It helps you to feel confident that you can weather *most* storms. Because the money is fairly liquid, think high yield savings account (HYSA) or a separate savings/checking account, you can readily access it in your time of need.

Why Do Teachers Need One? (Psst… Everyone Needs One!)

As a teacher, I go two plus months without an income. While I usually have built up cash from a bulk check paid at the end of the school year, it’s incredibly beneficial to not need to dip into those funds to pay for a broken A/C unit in my old Toyota Corolla or replace a set of tires after having a flat. It just makes sense. You don’t need to have a million bucks sitting around for emergencies, but you should have enough to weather small emergencies as they pop up.

So How Much Do I Need?

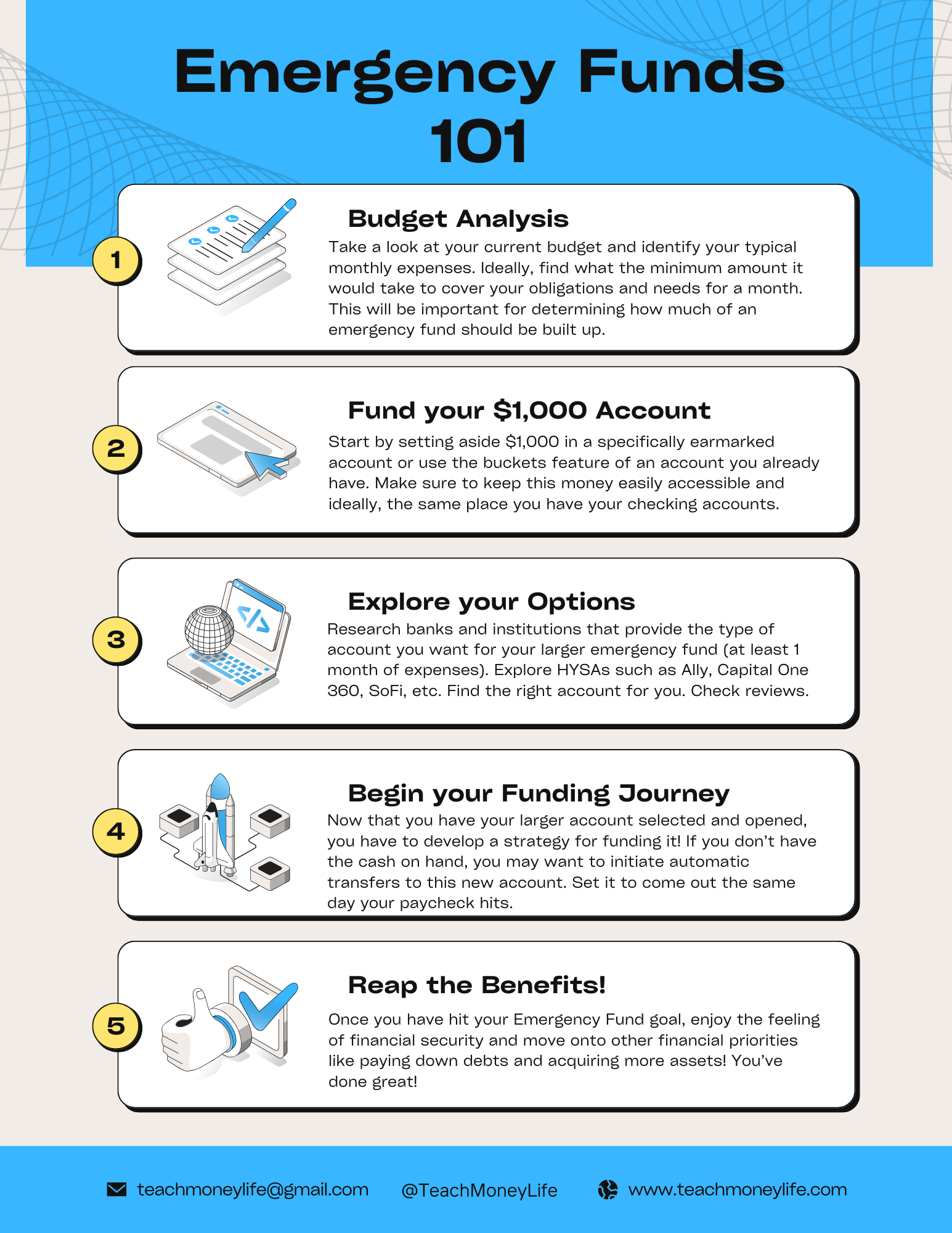

As Dave Ramsey would tell you, start with a $1,000 emergency fund. This should be one of the first things you build up when you are trying to right your financial ship.

And then you should try to build up that emergency fund to the equivalent of 3-6 months of essential expenses. This is the guideline often prescribed through basic personal finance education.

However… I would argue that it’s HIGHLY dependent on your situation, family size, and risk tolerance.

My general rule of thumb for my own expenses is that I need to have $1,000 in a savings account where my main checking account is housed and $10,000 in a high-yield savings account (HYSA). This gives me quick access to a small amount of cash immediately, and the ability to make a quick transfer up to $10,000 for larger emergencies. Additionally, keeping the bulk of that money in a HYSA lets it earn a much higher interest rate, and hopefully, lets it keep up with inflation.

Currently, my regular savings only provides a 0.05% interest rate, but my HYSA provides 3.8%.

Beyond that $11,000, I happen to have a taxable brokerage account (referral link to the brokerage I use) that I could access for backup cash if I was REALLY in need.

Why Not 3-6 Months of Expenses?

In my own personal experience, I want to have as much money in assets as possible. Since I also have a taxable brokerage account I can still access other money. If all my money was tied up in taxed advantaged accounts like a 401(K) or 403(b), then maybe I’d keep more liquid assets on hand. For our situation, my family could pay our fixed expenses and a basic food budget for about 2 months with our current emergency fund.

I am willing to risk being a bit short on an unexpected expenses or caught in a rough spot if I were to be out of work for multiple months. Part of that is that I believe the likelihood of such an need being relatively low, and part of it is that I want to maximize growth in my assets. By utilizing my taxable brokerage as a last case back up, I can let compounding build the account and if I ultimately must draw from that account, I will have built it up faster than just contributing to a low yield savings account.

Building Your Emergency Fund

Start small! Set a small weekly or biweekly contribution to a separate account earmarked for emergency savings. Depending on where you bank, you might have quick access to a HYSA for this initial emergency fund, which can help grow the size of the account a bit quicker. But ultimately this first step is more about your contributions than where the money is held.

$10/week will get you to $1,000 saved over the course of almost two years. While this isn’t really ideal, it’s infinitely better than having nothing or contributing nothing to your emergency fund. At bare minimum, you are building a habit of saving and paying yourself first, which will go a long way in improving your financial situation.

SHORTCUT– Make a few LARGE contribution by utilizing existing savings, funneling spare out of your paycheck or by finding some additional income to quickly get this one out of the way. If you typically spend $100/week on dining out, you can reallocate that outlay to reach a $1,000 account in just ten short weeks. If you can work a few additional hours and make an extra $250 a week, then you’ll be there in only FOUR weeks. It’s e

Once you’ve established your $1,000 emergency fund, you can start to tackle other things. If you are following Dave Ramsey’s Baby Steps, you can move into the debt snowball or debt avalanche pay down methods. Or if you are more risk averse or don’t have much debt, you can start to begin saving into a HYSA or other fairly liquid assets to build up to that $10,000 mark.

Hope This Helps!

I hope this quick walkthrough gets you thinking about starting an emergency fund or optimizing the amount and location of your current funds, and helps you make decisions to improve your financial life!

Now that you’ve finished, check out this FREEBIE to help keep you focused on the steps and your goal! And check out this page on four personal financial books all people should read!

{kind=link}